Bank Reconciliation: Definition, Example, and Process

If so, these entries will not appear in the bank reconciliation statement prepared at the end of the current month. Similarly, if a businessman deposits any checks on the last day of the month, these cheques may be collected by his bank and shown on his bank statement three or four days law firm accounting and bookkeeping 101 later. Similarly, some checks credited to the ledger account will probably not have been processed by the bank prior to the bank statement date. There are times when the bank may charge a fee for maintaining your account, which will typically be deducted automatically from your account.

Is your team struggling with time-consuming bank reconciliation?

The bank will debit your business account only when they’ve paid these issued checks, meaning there is a time delay between the issuing of checks and their presentation to the bank. These time delays are responsible for the differences that arise in your cash book balance and your passbook balance. Human error in the data entry process can sometimes lead to incorrect amounts or miscalculations on a business’s financial statements. While it cannot entirely erase the potential for data processing errors, using accounting software can reduce the likelihood of errors to help generate more accurate financial statements.

Helps in managing accounts receivables

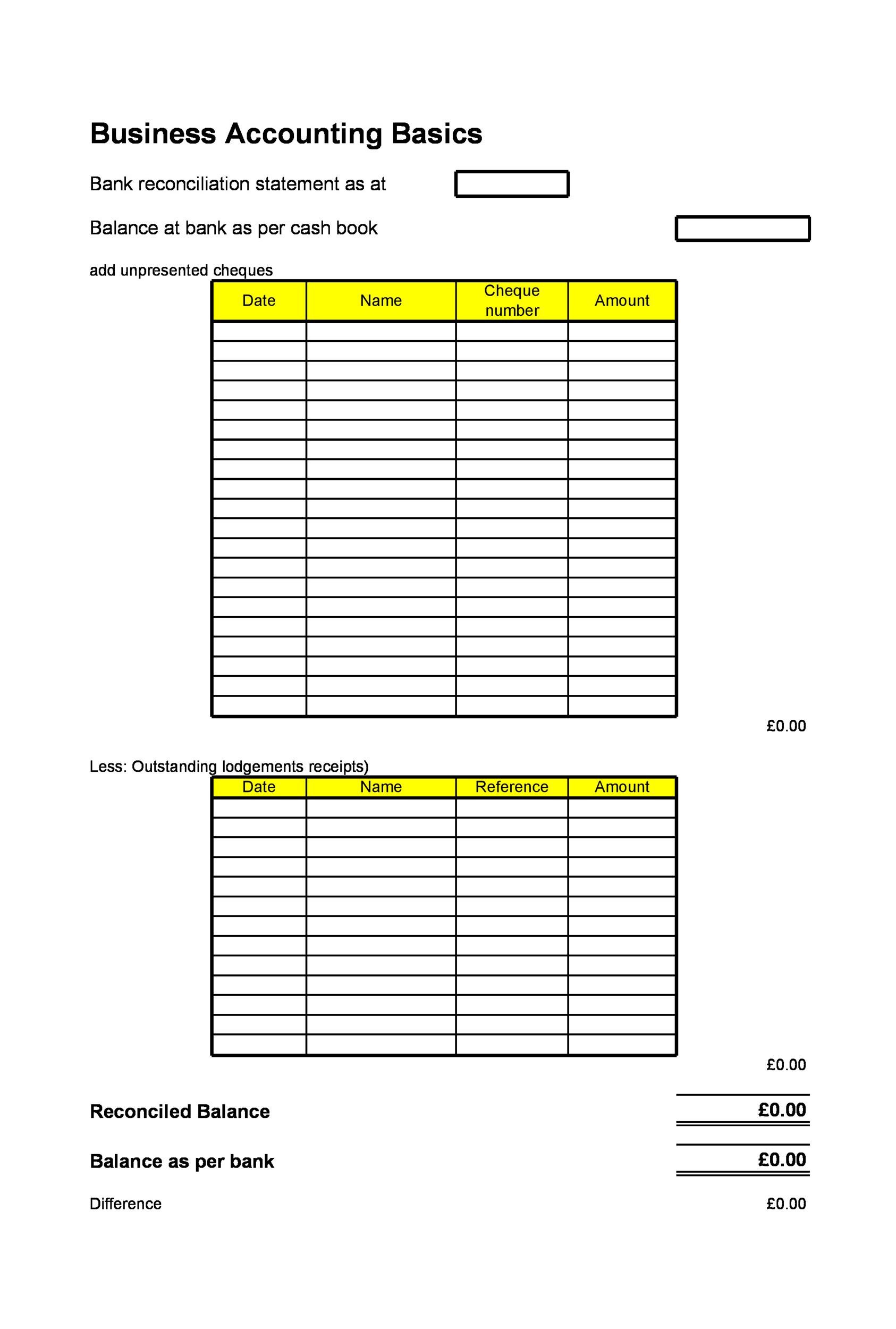

Find if there exists any debit memorandum that have not been recorded in your accounting record. Find all checks that you have issued but have not been presented for payment. You can do so by comparing the checks issued in your accounting record with the checks honored as per your bank statement.

Chasing overdue invoices draining your time?

A bank reconciliation reconciles the bank statement with the company’s bank account records. A bank reconciliation consists of a business’s deposits, withdrawals, expenses, and other activities directly impacting your bank account during a particular period. The purpose of this comparing and matching process is to ensure that discrepancies are identified and corrected. We’ll explore the definition of bank reconciliation, why it’s important, and a step-by-step process for performing bank reconciliations. We’ll also look at common sources of discrepancies between financial statements and bank statements to help you identify fraud risks and errors.

Someone on our team will connect you with a financial professional in our network holding the correct designation and expertise. This team of experts helps Finance Strategists maintain the highest level of accuracy and professionalism possible. Our team of reviewers are established professionals with decades of experience in areas of personal finance and hold many advanced degrees and certifications. Finance Strategists has an advertising relationship with some of the companies included on this website.

Reasons for Difference Between Bank Statement and Company’s Accounting Record

For large organizations and small businesses alike, a bank reconciliation should be prepared periodically because it enables you to report the most up-to-date figures. Knowing this information enables you to discover potentially nefarious activities, the bank administrator’s incompetence, or weaknesses in your reporting system in a timely manner. Additionally, many businesses are required by law to reconcile their bank accounts on a regular basis as part of their financial reporting obligations. The account holder is responsible for preparing a bank reconciliation to identify differences between the cash balance and the bank statements. You received $800 from Mr. Y (one of your debtors) on January 31, 2021 and recorded it immediately in your accounting records. You then sent this cash to your bank to be deposited into your account but it reached too late to be entered in your bank statement for the month of January.

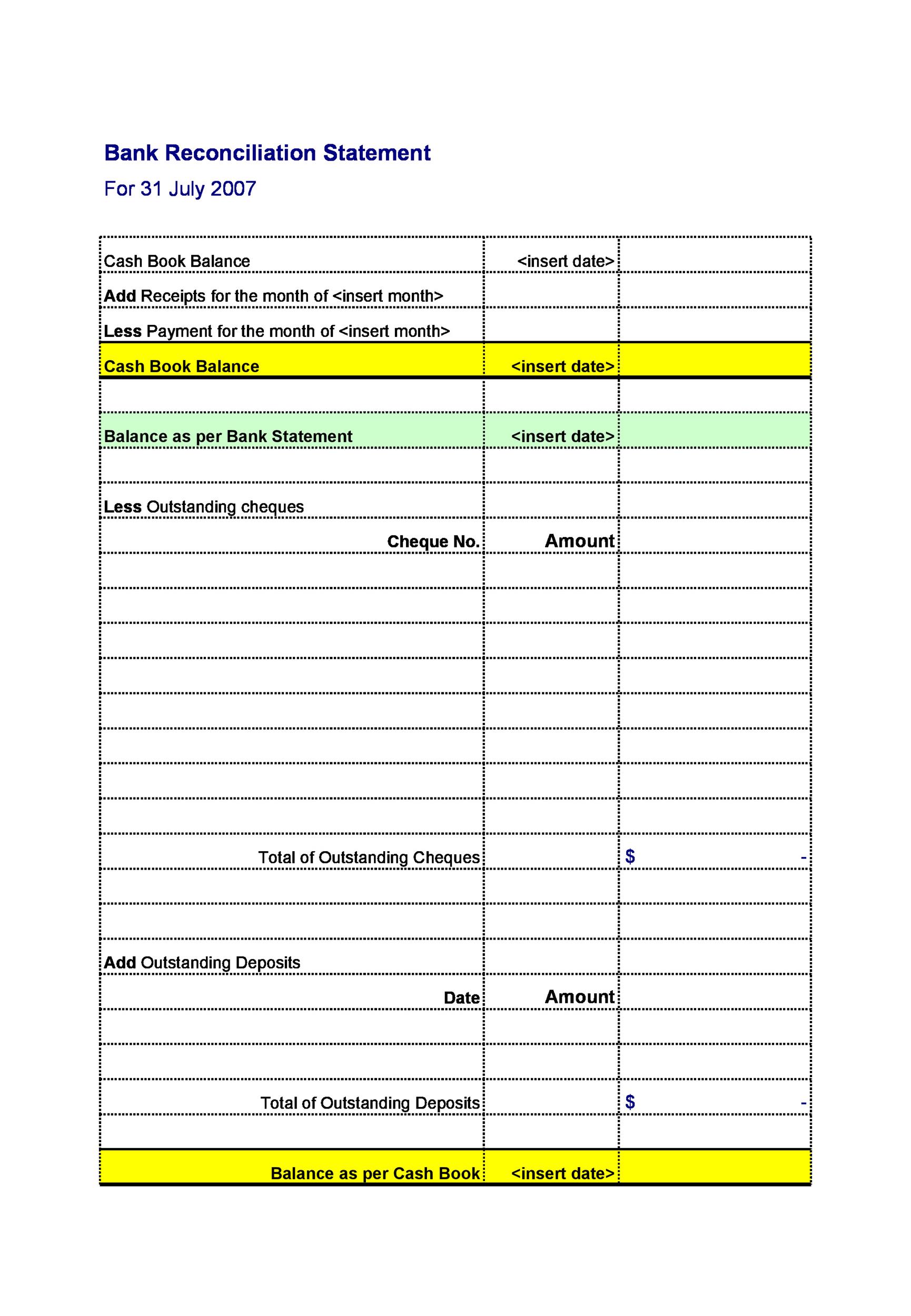

Bank statements also show expenses that may not have been included in financial statements, such as bank fees for account services. Notice that there are no journal entries posted for the bank statement adjustments (Step 1) because those are only used in the reconciliation process to calculate at the “correct” adjusted cash balance. The adjusted bank statement balance (5,300) is now equal to the adjusted cash book balance (5,300), so the bank reconciliation is complete. Bank reconciliation statements can help identify accounting errors, discrepancies and fraud. For instance, if the company’s records indicate a payment was collected and deposited, yet the bank statement doesn’t show such a deposit, there may have been a mistake or fraud. The company reflected the payment it received from debtors in its cashbook, but the payment hasn’t yet reflected in the bank account.

- At times, you might give standing instructions to your bank to make payments regularly on specific days to third parties, such as insurance premiums, telephone bills, rent, sales taxes, etc.

- If a company is unaware of the exact amount of these fees, they may not be included in the company’s financial records and will only be seen when they receive their bank statement.

- Theoretically, the transactions listed on a business’ bank statement should be identical to those that appear in the accounting records of the business, with matching ending cash balances on any given day.

- After recording the journal entries for the company’s book adjustments, a bank reconciliation statement should be produced to reflect all the changes to cash balances for each month.

- Thirdly, bank reconciliation helps to prevent errors that could lead to financial loss.

Nowadays, many companies use specialized accounting software in bank reconciliation to reduce the amount of work and adjustments required and to enable real-time updates. The source of bank statement entries is cheques deposited by customers, payments made to suppliers by issuing a draft or check. The source of cash book entries are deposits received from banks, cheques issued to creditors. Therefore, the bank credits the account holder’s personal account, and the entry appears in the Cr. Typically, each bank account is represented by a separate general ledger account. A reconciliation of this type would be prepared for each bank account and the cash records for that account.

At times, the balance as per the cash book and passbook may differ due to an error committed by either the bank or an error in the cash book of your company. It is important to note that it takes a few days for the bank to clear the checks. This is especially common in cases where the check is deposited at a different bank branch than the one at which your account is maintained, which can lead to the difference between the balances. To do this, businesses need to take into account bank charges, NSF checks, and errors in accounting.

It’s the duty of any business, large or small, to keep accurate financial records to ensure things balance. Next, check to see if all of the deposits listed in your records are present on your bank statement. Bank reconciliation helps to identify errors that can affect estimated tax payments and financial reporting. Bank issues a credit memorandum when it collects a note receivable on behalf of the depositor. Find if there exists any credit memorandum issued by the bank that you have not entered in your accounting record. If this interest is credited in the depositor’s account without intimating to depositor, the bank statement and the depositor’s record would not agree.

Compare the business’s financial records to the bank statement to spot the errors. This can be accomplished by matching transactions, and then adding or deducting any transactions that do not align to balance the total amounts. Company A paid $3,750 worth of checks into its bank account and debited its cash book accordingly, but the bank has not yet credited the funds to the depositor’s account. For example, if a business writes a check, it will post it to its cash book that day and then send it on to its supplier. The supplier will receive the check days later, and send it on to its bank. The check then passes through the banking system and eventually, a few more days later, it is processed by the bank of the business and posted to its account (bank statement).